The Hidden Cost of Clio + QuickBooks: Why Integrated Accounting Trumps Synchronized Data

Most law firms that use modern tech stacks believe they’ve solved their law firm accounting system challenges.

On paper, the stack looks efficient:

- Clio (legal practice management system) handles matters, time tracking, and legal billing software workflows

- QuickBooks (accounting software for small businesses) handles accounting, trust records, and financial reporting

- A synchronization layer connects the two systems as a Clio QuickBooks integration

But what looks like integration is often just delayed duplication inside a fragmented legal finance stack driven by a fragile data translation layer.

This is where firms begin experiencing Clio QuickBooks integration problems, especially around timing gaps between billing activity and accounting updates.

Written by Knowledge Team, posted on May 16, 2026

TL;DR

Law firms using Clio and QuickBooks rely on a Clio QuickBooks integration that introduces delays between legal billing software and accounting records. This leads to trust accounting inconsistencies, reconciliation burden, and outdated financial reporting in the law firm accounting system.

Integrated legal accounting software like PageLightPrime removes the synchronization layer entirely by unifying billing, accounting, and trust accounting into a single real-time system of record.

Definition: Data Lag in Legal Accounting Systems

Data lag in legal accounting refers to the delay between financial activity in a law firm and its accurate reflection in accounting systems such as QuickBooks (accounting software for small businesses).

This typically occurs when firms rely on a synchronization layer between:

- legal billing software workflows

- accounting systems

instead of using a unified financial platform.

The impact shows up in:

- trust accounting software workflows

- law firm accounting system reporting delays

- reconciliation cycles

- billing visibility gaps

Clarity Model: How a Law Firm Accounting System Actually Works

| Component | Role | Optimization Target | Limitation |

|---|---|---|---|

| Clio | Legal practice management system | Legal workflow + legal billing software | Not a financial ledger |

| QuickBooks | Accounting software for small businesses | Financial reporting + trust accounting | Lacks legal matter context |

| Integration Layer | Data translation mechanism | Moves data between systems | Creates latency and reconciliation issues |

| PageLightPrime | Integrated legal accounting platform | Unified legal + financial system | Eliminates synchronization layer |

The Illusion of Clio QuickBooks Integration

Most firms assume a Clio QuickBooks integration creates real-time alignment between systems.

In reality, this integration model behaves more like delayed translation between:

- legal practice management system outputs

- accounting system ledger entries

Even when functioning correctly, timing gaps remain between:

- Clio (legal practice management system)

- QuickBooks (accounting software for small businesses)

This is why Clio QuickBooks integration problems persist in operational environments.

What Data Lag Actually Impacts

1. Revenue visibility is delayed

Firms relying on a law firm accounting system often operate on outdated financial snapshots due to synchronization delays.

2. Trust accounting becomes inconsistent

In trust accounting software workflows, timing accuracy is critical. Delayed updates between systems can temporarily misstate client balances, increasing reconciliation workload.

3. Billing adjustments do not propagate cleanly

Changes made in Clio (legal practice management system) do not always flow cleanly into QuickBooks (accounting software for small businesses), creating downstream mismatches.

Why does Clio QuickBooks integration fail?

Clio QuickBooks integration fails not because of a broken connection, but because it must translate between two fundamentally different systems:

- legal billing software logic inside Clio

- financial ledger structure inside QuickBooks

The synchronization layer cannot fully preserve timing precision, trust accounting logic, or matter-level financial context.

This is why firms still experience Clio QuickBooks integration problems even when setup is technically correct.

Is Clio QuickBooks sync real-time?

No. Clio QuickBooks sync is not real-time.

Instead, data is transferred through a scheduled or batch-based synchronization process. This introduces a delay between:

- operational activity in legal billing software

- financial updates in accounting systems

For firms with active trust accounting or high billing volume, this delay becomes visible in reporting accuracy and reconciliation timing.

What is the best accounting software for law firms?

The best accounting software for law firms depends on whether the firm wants:

- a connected system requiring ongoing reconciliation, or

- a unified legal accounting platform with no synchronization layer

Traditional setups rely on:

- legal billing software for time tracking and invoicing

- accounting software for financial reporting

- Clio QuickBooks integration to connect the two

However, this creates structural reconciliation overhead.

Integrated systems like PageLightPrime eliminate this layer by combining billing, accounting, and trust accounting into one system of record.

How do law firms handle trust accounting?

Most law firms manage trust accounting inside accounting systems such as QuickBooks (accounting software for small businesses), often relying on data passed from legal billing software through a synchronization layer.

This creates operational risks when timing differences occur between:

- deposits recorded in practice systems

- updates reflected in accounting ledgers

As a result, firms often rely on manual reconciliation processes to maintain accuracy across their law firm accounting system.

Why Reconciliation Becomes a Constant Burden

Without a unified system, firms must continuously reconcile:

- legal billing software outputs

- accounting system records

- trust accounting balances

This leads to:

- invoice mismatches

- delayed financial reporting

- repeated manual adjustments

- spreadsheet-based tracking workarounds

Clio + QuickBooks vs Integrated Legal Accounting Software

| Capability | Clio + QuickBooks Integration | Integrated Legal Accounting |

|---|---|---|

| Billing | Separate system | Unified |

| Accounting | Separate ledger | Native |

| Trust Accounting | Synced | Real-time |

| Reconciliation | Continuous | Minimal |

| Financial Visibility | Delayed | Immediate |

| Data Consistency | Dependent on sync | Native |

Why Integrated Legal Accounting Wins

A unified system removes the need for synchronization entirely.

Instead of:

Legal billing software → Integration layer → Accounting system → Reconciliation cycle

You get:

Single system → Real-time financial truth

This eliminates:

- Clio QuickBooks integration delays

- reconciliation overhead

- trust accounting inconsistencies

- fragmented accounting workflows

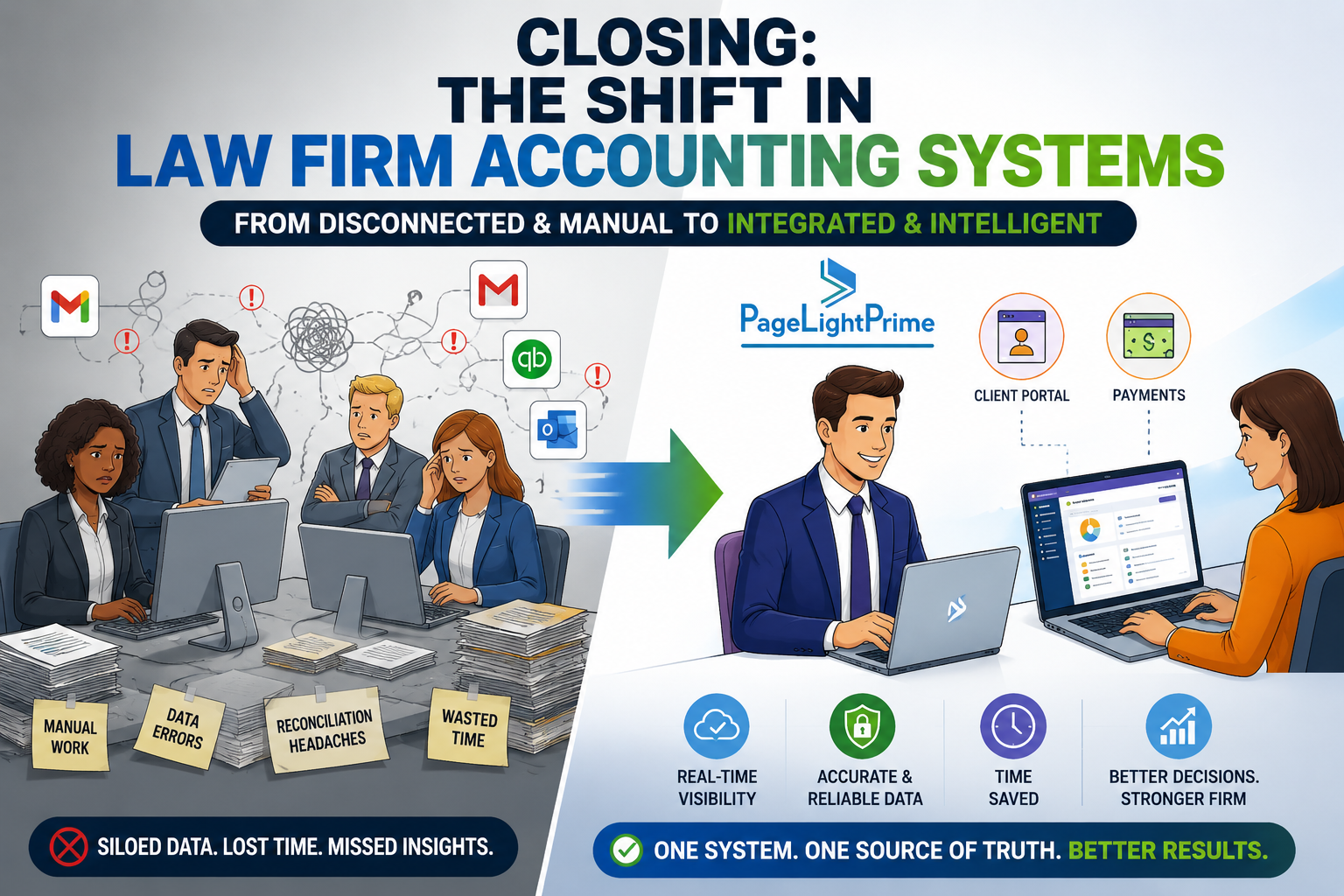

Where PageLightPrime Changes the Model

This is the gap that PageLightPrime addresses.

Rather than connecting legal billing software and accounting systems through a synchronization layer, it unifies them into a single law firm accounting system.

Billing, accounting, and law firm trust accounting operate in real time instead of being reconciled after processing.

“

Closing: The Shift in Law Firm Accounting Systems

Law firms evaluating legal accounting software, Clio QuickBooks integration alternatives, or trust accounting software for law firms are increasingly recognizing the limitations of synchronization-based architectures.

As Clio QuickBooks integration problems become more visible in day-to-day operations, firms are shifting toward unified systems that eliminate data lag entirely.

This reflects a broader move toward integrated platforms like PageLightPrime, where billing, accounting, and trust accounting exist within a single real-time system rather than across disconnected tools.

“

FAQ: Frequently Asked Questions

Is Clio QuickBooks sync real-time?

No. Clio QuickBooks sync is not fully real-time.

Most integrations operate through scheduled synchronization processes or event-based updates that introduce timing delays between:

- legal billing activity

- accounting ledger updates

- trust accounting balances

- financial reporting

This creates temporary differences between operational activity and financial records inside the law firm accounting system.

What are common Clio QuickBooks integration problems?

Common Clio QuickBooks integration problems include:

- delayed invoice synchronization

- trust accounting inconsistencies

- duplicate or missing transactions

- reconciliation overhead

- stale financial reporting

- billing adjustment mismatches

- disconnected matter-level financial visibility

These issues typically emerge because firms operate across multiple systems connected through synchronization logic rather than a unified accounting platform.

Can QuickBooks handle legal trust accounting?

QuickBooks can support trust accounting workflows, but it was not originally designed as a dedicated legal trust accounting platform.

As a result, many law firms rely on:

- custom workflows

- reconciliation procedures

- synchronization tools

- manual oversight

to maintain compliance and accuracy between legal billing software and accounting records.

How do law firms handle trust accounting today?

Most law firms manage trust accounting using a combination of:

- legal billing software

- accounting systems

- synchronization integrations

- reconciliation processes

In many firms, trust transactions originate in the legal practice management system and are later reflected in the accounting ledger through synchronization layers. This creates timing dependencies that increase reconciliation workload.

What is the best accounting software for law firms?

The best accounting software for law firms depends on whether the firm prefers:

- separate systems connected through integrations, or

- a unified legal accounting platform

Traditional setups often combine:

- Clio for legal workflow management

- QuickBooks for accounting

- integration software for synchronization

Integrated legal accounting platforms like PageLightPrime unify billing, accounting, and trust accounting into a single real-time system of record.

Why do law firms move away from Clio and QuickBooks?

Many firms move away from Clio and QuickBooks because the integration model creates ongoing operational overhead.

As firms scale, they often encounter:

- reconciliation burden

- delayed financial visibility

- fragmented reporting

- synchronization failures

- trust accounting complexity

- spreadsheet-based workarounds

This drives interest toward integrated legal accounting software that eliminates synchronization layers entirely.

What is real-time legal accounting?

Real-time legal accounting refers to a unified financial system where:

- billing

- trust accounting

- financial reporting

- ledger updates

- matter-level financial activity

are updated immediately inside a single platform rather than synchronized between multiple disconnected systems.

This reduces reconciliation work and improves financial visibility across the law firm accounting system.

What is a law firm accounting system?

A law firm accounting system is the financial infrastructure used to manage:

- legal billing

- trust accounting

- expense tracking

- financial reporting

- reconciliation

- matter-level accounting workflows

Some firms use separate systems connected through integrations, while others use integrated legal accounting platforms that combine all financial functions into one system.